End-of-Lease Options Explained: Renew, Return, or Buy

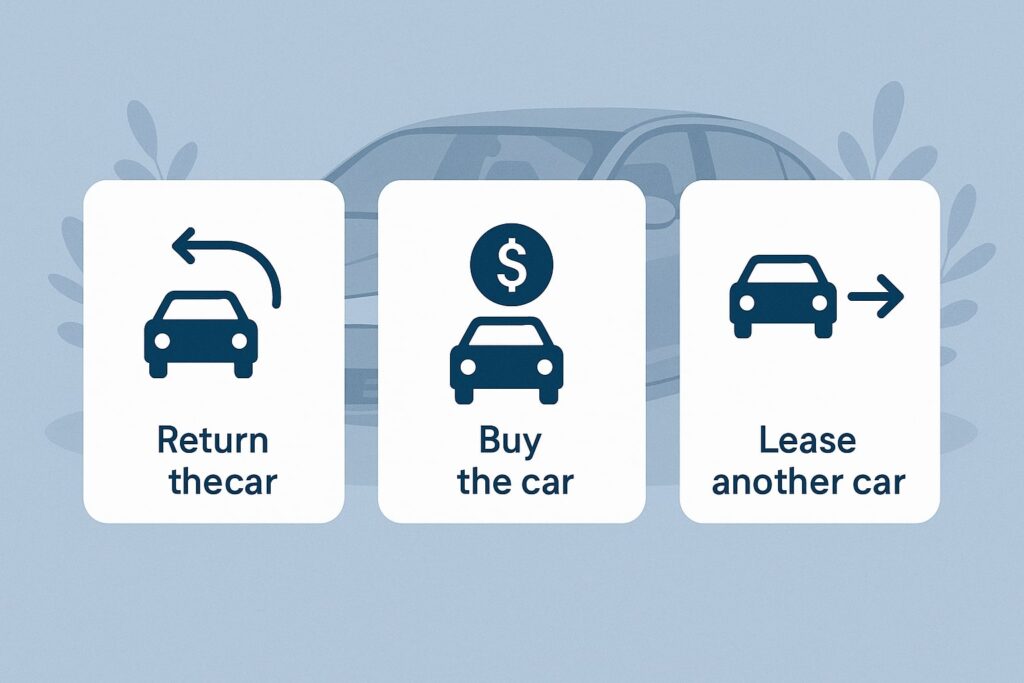

When a lease term ends – whether on a car, machinery, or office equipment – you typically have three paths: renew/extend the lease, return the asset, or buy it. These “end-of-lease options” determine your next move.

As one industry guide notes, “a lessee has three choices: return the equipment, renew the lease, or purchase the equipment”.

For example, about a quarter of new cars are leased in the US, meaning millions of vehicles and assets reach lease-end each year. This article breaks down each option so you can choose wisely.

Understanding End-of-Lease Choices

A lease is a contract giving you (the lessee) the right to use an asset for a set time in exchange for payments. When that term ends, an end-of-lease option clause in the contract typically spells out your choices.

Return (or walk away) means handing the asset back with no further use; Renew (or extend) means signing a new lease or a short extension; Buy means paying a predetermined price (the residual value) to own the asset.

Civista Bank’s leasing guide defines these end-of-lease options clearly: at term’s end, you can return the equipment, renew the lease, or purchase the equipment. The residual value (or purchase option price) is usually set when you start the lease, reflecting the asset’s estimated worth at lease-end. It’s crucial to locate this number in your contract early on.

How these options play out can depend on lease type. For example, a fair market value (FMV) lease (common in equipment financing) explicitly lets you “purchase the leased equipment at its fair market value, return the equipment, or renew the lease”.

In a capital lease or “$1 buyout” lease, the contract is structured so you effectively own the asset at the end (often for a nominal final payment). Whether personal or business lease, the fundamental choices remain return, renew, or buy.

Option 1: Renew (Extend) Your Lease

If you still need the asset and want to avoid a big upfront outlay, you may renew or extend the lease. Renewing typically means signing a new lease term on the same item, possibly with updated monthly payments or length.

“Renewing the lease involves extending the current agreement for a specified period,” notes PNC’s equipment leasing guide. This is beneficial if the equipment still meets your needs and you prefer not to purchase new gear outright.

- Lower up-front cost: You avoid the large cash payment required to buy. PNC explains that renewing “can be beneficial if the equipment still serves operational needs and the lessee prefers not to make a substantial up-front investment”.

- New negotiation: A renewal is an opportunity to renegotiate terms. For example, you might get a new monthly rate or extended term that better fits your plans.

- Keep known assets: You retain an asset you’re already familiar with, avoiding the disruption of switching to new equipment or a different vehicle.

However, renewing means continued costs and older technology. You’ll keep paying monthly fees, and the asset may be aging. For car leases, dealers often allow a month-to-month extension if you haven’t found a new vehicle in time.

That means continuing payments under essentially the same contract until you decide. In any case, before renewing, check current market deals – sometimes leasing a brand-new model can be cheaper than another extension.

When to renew: If your needs haven’t changed (you still use the item heavily) and newer versions aren’t a big priority, an extension can make sense.

It’s also a way to buy more time while you shop around. Just confirm that the equipment’s remaining useful life still aligns with your plans and that you won’t be paying too much for older equipment.

Option 2: Return (Walk Away)

Walking away means returning the asset to the lessor when the lease ends. This is often the simplest route, especially if you no longer need the item or want something new.

As PNC notes, “returning leased equipment is often the most straightforward option”. For many car lessees, returning the car at lease-end is the typical choice.

- No further obligations. You hand back the asset and stop payments (aside from any end fees). PNC advises that returning is ideal “if the equipment no longer meets operational needs, or if the business is planning to upgrade to newer technology”.

- Upgrade opportunity. Returning lets you lease or buy a newer model. You’re free to shop for an upgrade without being tied to your old unit. In a car context, this means you can walk into any dealer and get a fresh lease or purchase.

- Avoids ownership hassles. You don’t need to worry about selling the old asset later or paying for long-term maintenance.

However, returning often incurs end-of-lease fees and charges. For vehicles, expect a disposition fee plus any charges for excess mileage or wear-and-tear. PNC similarly cautions to “ensure the equipment meets the lessor’s return conditions” to avoid extra penalties.

For example, scratched paint or missing parts on equipment (or dings on a car) can trigger fees. Make sure to inspect and repair the item if needed before returning.

- Logistics and timing. You’ll need to coordinate physically returning the asset (driving it back, shipping equipment, etc.). PNC notes factoring in “logistics of returning the equipment, such as transportation and timing”. Plan ahead so you’re not scrambling on the final lease day.

- No more use. Once returned, you lose access immediately. If you still need that car or machine, you must secure a replacement quickly.

When to return: If your asset is outdated, surplus to your needs, or you simply want the flexibility to move on, returning is sensible. It’s often chosen by lessees who want a clean break. Just prepare for any fees by reviewing the lease’s fine print on condition requirements, and consider lining up your next vehicle or equipment in advance.

Option 3: Buy the Asset (Lease Buyout)

Buying means taking ownership of the asset by paying the lease buyout price (often the residual value). At lease-end you have the option to purchase the asset for a set price. This can be done at the end of the lease, or sometimes even early if the lessor allows a buyout.

- Predetermined price. The contract’s residual value (or purchase option) is the amount you’d pay to buy it.

For example, Kelley Blue Book explains that the residual is “the estimated amount the vehicle is worth at the end of the lease…it’s the buyout price”. This number is fixed in your agreement, so you know it ahead of time. - Equity in the asset. If the asset’s market value exceeds the residual, you effectively have built “equity”. In that case, buying can be a bargain.

Experts advise crunching the numbers: “if your car’s residual value is lower than the current market value for that model,” you might profit by buying it. For instance, if a leased truck’s buyout is $20,000 but similar trucks sell for $23,000, you have $3,000 of equity. - Ownership benefits. Once bought, you no longer owe lease payments. You can modify or use the asset freely.

For businesses, owning equipment may allow claiming additional tax deductions (like depreciation) that aren’t available when leasing. For a car, you could keep it indefinitely or sell it on your own terms later.

However, buying requires cash or financing and assumes risks:

- Large payment or loan. You must pay the buyout price in cash or take out a loan. Even if you finance it, you’ll likely pay interest. Kelley Blue Book notes that “you’ll save on interest charges if you can pay cash” at lease-end.

- Potential overpayment. If the residual is higher than market value, buying is a poor deal. KBB warns “the buyout option isn’t a good choice if the car’s residual value is higher than the market value”. In that case, you’d overpay for an aging asset. Always compare the contract price to current ads for similar models.

- Older technology. If it’s an older model (e.g. a 3-year-old machine), it may lack new features or efficiency. Buying might lock you into maintenance costs. As one source notes, renewal or return may be better “if the leased equipment must be regularly updated” and you don’t need the old model forever.

When to buy: Consider purchasing if you love the asset and it’s in great shape, or if dealers are quoting high prices for replacements. For example, KBB suggests buying if “you like the [vehicle] you’ve been driving and if it can be bought for significantly less money than a comparable model”.

Also, in some markets where new models are scarce, buying may avoid long waits. Just run the math: compare total cost of buying (price + interest) vs leasing new or buying another on the open market. If there’s equity (asset worth > buyout price), you even stand to pocket the difference by selling it later.

One thing to watch for: in certain U.S. states, sales tax can apply when buying a leased vehicle. For instance, CarPro warns that in Texas and California, lessees must purchase the car first and pay sales tax on that sale, which can eat into any equity. Always check local tax rules before deciding to buy a lease.

Comparing the Options

Choosing among renew, return, or buy depends on your situation. The table below summarizes when each option makes sense and its pros and cons:

| Option | How it Works | When It’s Best | Pros and Cons |

|---|---|---|---|

| Renew/Extend | Extend the lease (sign a new term) on the same asset. | – You still need the asset. – No budget for a big purchase. – Newer models not needed. | + Keeps using the same asset (no switch needed). + Avoids large outlay. + Can renegotiate terms. – Still pay monthly fees. – Keeps older tech/asset. – Leasing costs add up over time. |

| Return | Give the asset back to the lessor (end the lease). | – Asset is outdated or unneeded. – You want a fresh replacement. – You have no desire to own it. | + No more payments (except end fees). + Freedom to choose a new model or deal. – Disposition, wear-and-tear, and mileage fees. – Loss of any lease equity. – Must find a replacement if still needed. |

| Buy (Buyout) | Pay the residual price to purchase and own the asset. | – Asset still useful long-term. – You like its condition or features. – Buyout price is a good deal (residual < market). | + You own the asset (no further lease costs). + Possibly a bargain if market value is higher. – Requires cash or financing. – Can overpay if residual > market. – Asset may soon need upgrades. |

Key Considerations

Before deciding, weigh these critical factors (experts recommend analyzing them carefully):

- Costs and Cash Flow: Compare the total cost of buying versus leasing. Consider monthly payments, any required down payments, financing costs, and end-of-lease fees. For businesses, also factor in tax implications.

As PNC advises, “analyze cash flow implications and tax benefits associated with each option”. If buying, can you afford it now? If renewing, are the payments manageable? - Asset Condition and Life: How much useful life is left in the asset? If it’s nearly worn out or obsolete, returning makes sense.

The lease agreement terms should reflect this – for example, FMV leases are often used for equipment expected to become outdated. Team Financial suggests asking: “What is the remaining life of the equipment?” and “Would a newer model improve operations?”. - Operational Needs: Do your needs justify keeping or upgrading? If your current asset still does the job well, renewing or buying might save you the hassle of transitions.

Conversely, if new technology could dramatically boost efficiency, it might be worth returning and leasing/buying anew. Think of “whether newer equipment offers enhanced productivity or cost savings”. - Market Value vs Residual: If considering purchase, use pricing tools or dealer quotes to estimate current market value.

Kelley Blue Book encourages lessees to compare the contract’s residual value to what the asset would fetch on the open market. If the market price is higher, you have equity and buying is advantageous. If it’s lower, you’d overpay by buying. - End Fees and Penalties: Review your lease paperwork for any fees. Common costs include disposition fees (for ending the lease), charges for excess usage, and repair costs to meet return conditions. If you have equity, you might avoid some fees by purchasing or trading in.

- Timing and Planning: Start evaluating at least a few months before lease-end. CarPro advises reviewing your lease about 120 days out so you understand the numbers (residual, true market value) and timeline.

Likewise, see if you can extend month-to-month (PNC notes this may be possible) while you decide.

By strategically weighing these factors, you can optimize your decision. For instance, PNC suggests minimizing disruption and ensuring any upgrade truly adds value.

Team Financial Group highlights questions like comparing leasing versus buying costs and planning for future needs. In practice, businesses often balance financial calculations with operational goals – which leads to the option that best fits their situation.

Frequently Asked Questions

Q.1: What are my end-of-lease options?

Answer: When a lease ends, you generally have three paths:

(1) Return the asset and walk away (possibly leasing or buying something new), (2) Renew/Extend the lease for more time, or (3) Buy the asset (exercise the purchase option). In equipment leasing terms, as one guide puts it, those options are to return, renew, or purchase the equipment.

Q.2: How do I decide which option is best?

Answer: It depends on cost and needs. Calculate the total cost of each choice (lease more, return and replace, or buyout). Check if the asset’s market value is above the contract’s buyout price – if so, buying could be a bargain.

Also consider whether you still need the equipment (renew) or want to upgrade (return). A good rule is: if the buyout price is a good deal (lower than comparable used price), buying may make sense; otherwise, returning or renewing could be smarter.

Q.3: What does “residual value” mean?

Answer: Residual value is the pre-set amount you must pay to buy the leased item at lease-end. It’s calculated by the lessor at lease inception as the asset’s expected worth later.

For example, if your leased copier has an MSRP of $10,000 and the residual is 50%, you’d owe $5,000 to buy it. Comparing this value to the asset’s actual market value today helps determine if you have equity.

Q.4: How much are the fees if I return the leased item?

Answer: Common charges include a disposition fee (for closing the lease), plus penalties for excess use. For vehicles, expect fees for going over the mileage limit and for any excessive wear or damage.

For equipment, check the lease’s return condition clauses – you might pay for refurbishing or shipping. Always inspect the item against the lease’s return checklist to avoid surprises.

Q.5: Can I extend my lease beyond the original term?

Answer: Often yes. Many lessors allow a short extension or month-to-month arrangement if you need more time. Kelley Blue Book notes that most leasing companies will “extend the lease month-to-month or for a fixed number of months” if you haven’t replaced the item.

This means you keep paying roughly the same amount under a short-term extension. You’ll likely sign a simple addendum rather than a whole new lease, but always check with your lessor well before the term ends.

Q.6: When should I start preparing for the lease-end?

Answer: Begin planning a few months in advance. For vehicle leases, 3–4 months (around 120 days) before your lease ends is recommended. Pull out your contract and identify key numbers: the residual (buyout price) and any fees.

Research current market prices for similar assets. Early prep lets you compare options calmly and avoid last-minute pressure.

Q.7: Are there tax implications in choosing an option?

Answer: Possibly. Lease payments for business equipment are often tax-deductible as regular expenses, whereas buying might let you depreciate the asset. For vehicles, sales tax may apply if you buy it out (often calculated on the purchase price).

In fact, some states require paying sales tax when you buy a leased car. Check with a tax advisor: generally, operating leases offer upfront write-offs, while capital leases (or buyouts) affect depreciation schedules. The best choice may hinge partly on your tax situation.

Conclusion

Facing the end of a lease means evaluating your goals and resources. Renewing lets you keep using the asset with no big upfront cost; returning frees you to upgrade or downsize with minimal commitment; buying grants ownership if the price is right. Each path has advantages and trade-offs.

Experts agree that the smart move is to analyze all factors—financial, operational, and market—before deciding. By weighing costs, asset condition, and your future needs, you can choose the option that best supports your plans and budget.

Ultimately, the right end-of-lease decision aligns with your situation. As industry guides advise, carefully compare cash flow and tax effects, minimize disruption, and ensure any upgrade justifies its cost. With thoughtful preparation and a clear understanding of these options, you’ll navigate the lease-end with confidence.