Understanding Credit Score Requirements for Equipment Loans

Qualifying for equipment financing can feel confusing, especially when lenders emphasize credit. In the U.S., credit score requirements for equipment loans influence your interest rate, down payment, and approval odds.

This guide breaks down how scores are used, what lenders look for beyond a number, and practical steps to qualify. You’ll learn the differences among banks, credit unions, online lenders, and SBA-backed options, plus ways to structure a deal if your credit is still building.

Throughout, we’ll keep the language simple, the advice actionable, and the information tailored for U.S. borrowers—from sole proprietors to growing LLCs and corporations—so you can navigate credit score requirements for equipment loans with confidence.

What Counts as an “Equipment Loan” and Why Credit Scores Matter

An equipment loan is a financing product used to purchase hard assets for business use, such as trucks, excavators, CNC machines, restaurant ranges, medical devices, or POS systems.

The equipment itself typically serves as collateral, which is why equipment loans are often easier to approve than unsecured business loans. Still, credit score requirements for equipment loans remain central because a score predicts the likelihood of on-time repayment.

Lenders use your credit score to price risk, decide on loan-to-value (LTV), and determine whether a personal guarantee (PG) is required. Even when the equipment is highly resalable, a weak score can trigger higher rates, shorter terms, or a larger down payment.

In practice, lenders blend personal and business credit data. Newer businesses often rely primarily on an owner’s FICO score, while established firms may be evaluated with business credit bureaus like Experian Business, Equifax Business, or Dun & Bradstreet (D-U-N-S, PAYDEX).

If your company is young, your personal score may carry more weight; if you’re seasoned with strong financials, business credit can play a bigger role. Either way, credit score requirements for equipment loans shape the overall approval, but they rarely operate alone—cash flow, time in business, and collateral value matter just as much.

How Equipment Loans Are Structured and How That Affects Your Credit Profile

Equipment loans are usually term loans with fixed monthly payments, though leases and lease-to-own contracts are also common. The structure affects your application. A traditional term loan finances a percentage of the invoice price—often 80% to 100%—with the equipment as collateral.

A finance lease may offer tax and accounting benefits, with a nominal (or stated) purchase option at the end. In both structures, credit score requirements for equipment loans intersect with LTV and term length.

Higher scores can unlock longer terms, lower payments, and smaller down payments, improving your debt-service coverage ratio (DSCR).

Most lenders file a UCC-1 financing statement on the equipment. That filing is normal, but if your credit profile already shows multiple UCC liens, a lender might view you as over-leveraged.

Likewise, if your personal credit shows maxed-out cards or recent late payments, an underwriter may request a co-borrower, a bigger down payment, or proof of contract revenue.

This is why credit score requirements for equipment loans are best considered alongside a broader readiness checklist: clean personal credit, organized business financials, and a clear plan for how the machine drives revenue.

Types of Equipment Financing and How Each Handles Credit Risk

There are three common formats: term loans, capital/finance leases, and operating leases. Term loans are straightforward: you borrow against the equipment, pay interest and principal, and own the asset outright.

Capital leases behave similarly for accounting purposes and may end with a $1 buyout or stated residual. Operating leases emphasize use rather than ownership and may carry lower payments, but the lender retains more control at term end.

The credit score requirements for equipment loans vary with structure; operating leases sometimes accept slightly lower scores because the lender expects to recover value by re-leasing equipment. Finance leases and loans may ask for higher scores if the asset is specialized or depreciates quickly.

Industry matters too. For example, long-haul trucks have robust resale markets, which can offset marginal credit. Niche medical devices or custom machines may require stronger credit or larger down payments.

If your credit is borderline, you may improve approval odds by choosing equipment with stable resale value, negotiating a manufacturer discount to reduce the financed amount, or agreeing to maintenance and insurance terms that protect the collateral.

In every case, credit score requirements for equipment loans guide pricing, but smart structuring often bridges the gap.

Understanding FICO vs. VantageScore and What Lenders Actually Pull

Most lenders rely on FICO models because they’re deeply entrenched in commercial credit policies. VantageScore is also used, especially by some fintechs, but underwriting playbooks are usually written around FICO 8, FICO 9, or a bank’s preferred version.

Regardless of model, credit score requirements for equipment loans focus on the same levers: payment history, utilization on revolving trade lines, age of accounts, types of credit, and inquiries.

Underwriters also read your credit report narrative—late payments on auto loans or installment debt can weigh more heavily for equipment financing than, say, a single late retail card.

If you operate as a sole proprietor, expect your personal score to be decisive. If you own an LLC or S-Corp with established business credit and clean financials, the lender may pull both business and personal credit. For owner-guaranteed loans, a minimum FICO threshold is common, even when business credit is strong.

To meet credit score requirements for equipment loans, it’s wise to monitor both personal and business profiles: ensure your business address, legal name, and EIN are consistent across vendors and bureaus, and keep vendor terms current so on-time payments populate your file.

Why Personal Credit Still Matters for Business Equipment Financing

Even mature companies can be asked for a personal guarantee, especially in smaller deals (e.g., $25,000–$250,000) or when the equipment is specialized. From a lender’s perspective, a PG aligns incentives and adds a secondary source of repayment if the business struggles.

Consequently, credit score requirements for equipment loans often read like personal-credit guidelines: a 700+ FICO might target the best rates, while 660–699 can still be competitive with solid financials. Scores below the mid-600s may still qualify, but expect bigger down payments and higher APR.

Personal credit also reflects your habits: low utilization, long credit history, and no recent delinquencies indicate discipline—qualities underwriters prize. If you anticipate applying within six months, avoid opening unnecessary new credit lines and keep card balances well below 30% of limits, ideally under 10%.

Paying down revolving balances just before the statement cuts can boost the reported score at the right moment, helping you surpass credit score requirements for equipment loans without changing your overall finances.

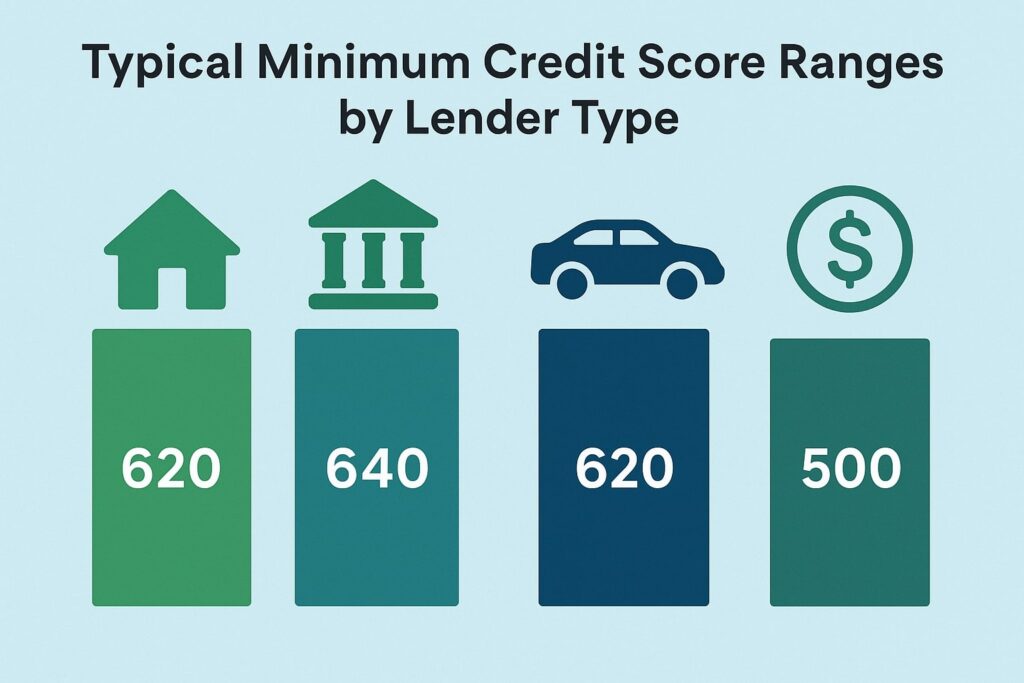

Typical Minimum Credit Score Ranges by Lender Type

Credit policy varies by lender, industry, and deal size, but patterns exist. Traditional banks usually prefer higher scores and deeper financials. Credit unions can be flexible with members. Online lenders often trade higher rates for speed and broader approvals.

Captive financing arms (offered by manufacturers) may run promotions. And SBA-backed loans blend private lender underwriting with government guarantees.

Understanding these lanes helps you target the best fit for your profile and the credit score requirements for equipment loans you’re likely to meet.

Banks and Credit Unions: Strongest Rates, Stricter Credit

Banks and credit unions generally look for FICO scores in the high-600s to 700+ range, especially for unsecured risks or longer terms.

For secured equipment deals with predictable collateral, some banks will evaluate applicants in the mid-600s if cash flow is strong and the down payment is meaningful. But banks also scrutinize DSCR (often targeting 1.25x or higher), time in business (2+ years preferred), and liquidity.

While their credit score requirements for equipment loans are not the only hurdle, traditional institutions expect clean personal credit: limited late payments, no recent charge-offs, low credit utilization, and minimal hard inquiries.

Credit unions can be more relationship-driven. If you’ve maintained accounts in good standing, you may access friendlier terms even if your score sits slightly below a bank’s comfort zone.

Still, they’ll evaluate the whole package—equipment type, LTV, guarantor strength, and existing debt. To position yourself well, present three years of financials if available, current interim statements, and clear projections showing how the equipment generates revenue.

Pairing strong documents with a solid score helps satisfy credit score requirements for equipment loans at these institutions.

Online and Alternative Lenders: Broader Approvals, Faster Decisions

Online lenders and specialty finance companies often approve applicants with scores in the low- to mid-600s, sometimes even lower for exceptionally strong collateral or revenue. In exchange, pricing typically rises, and terms may be shorter.

These lenders excel at speed: approvals can arrive within hours once you submit bank statements and the equipment quote. Their credit score requirements for equipment loans are more flexible, but they lean heavily on cash-flow data pulled from your business bank account, daily balances, and deposit patterns.

Expect them to verify time in business, average monthly revenue, and NSF frequency. They’ll also assess whether the equipment has a robust resale market.

If your score is sub-prime, you can strengthen your application with a 10%–30% down payment, a co-signer, or by pledging additional collateral. While you may pay more, fast funding can make sense when a contract opportunity hinges on acquiring a machine quickly.

Use these lenders strategically to build credit and refinance later as your profile improves, aligning your path with stricter credit score requirements for equipment loans over time.

Captive Finance (Manufacturer Programs): Promotions and Flexibility

Captive finance arms—like those affiliated with major equipment brands—design programs to sell more units. They may offer promotional rates, deferred payments, or seasonal structures aligned with your industry.

Their credit score requirements for equipment loans can be competitive because they’re motivated by equipment sales, not just loan yield. For standard promotions, a mid-600s score with strong revenue can be enough, especially if the asset is a mainstream model with a stable resale market.

Captives also understand the asset better than generalist lenders. If you’re buying a new excavator or an FDA-approved device with predictable lifespan and service records, they can underwrite with confidence.

Bring documented maintenance plans and warranty details; these can offset slightly lower credit scores by reducing perceived risk. If you’re marginal on credit, ask the dealer about “subvented” programs where the manufacturer helps lower the rate.

These programs are designed to smooth credit score requirements for equipment loans while keeping total cost of ownership attractive.

SBA-Backed Options: Strong Documentation, Wider Access

SBA 7(a) loans can finance equipment as part of broader working-capital needs, and SBA 504 loans are built for fixed assets like machinery and owner-occupied real estate. While SBA does not publish a universal minimum FICO, participating lenders commonly look for scores in the mid- to high-600s with clean histories.

The government guarantee reduces lender risk, which can help applicants who narrowly miss conventional credit score requirements for equipment loans. Expect rigorous documentation, including business plans, multi-year financials, and detailed use-of-funds.

SBA deals take longer to close but can deliver longer terms and competitive rates, improving DSCR. The 504 structure—pairing a bank first lien with a CDC second—can support large purchases with modest down payments.

If your credit is fair but your business is stable, SBA may be the bridge to ownership. Prepare early, respond quickly to document requests, and show how the new equipment expands capacity, revenue, or margins.

That narrative, supported by data, helps offset borderline credit and aligns with lenders’ credit score requirements for equipment loans.

Beyond the Score: What Underwriters Evaluate (Cash Flow, DSCR, LTV, and Collateral)

Underwriters don’t approve a number; they approve a story supported by data. They look at revenue consistency, operating margins, and free cash flow to confirm a DSCR of at least 1.20x–1.25x after the new payment.

They evaluate LTV—often targeting 80%–100% depending on asset class—and they consider the equipment’s age and expected useful life.

The credit score requirements for equipment loans intersect with these metrics: a higher score can justify higher LTV or longer terms, whereas a lower score may require more equity and shorter amortization to keep risk in check.

Bank statements matter more than many applicants realize. Lenders scan for daily balances, deposit volatility, and overdrafts. Even with a solid score, frequent NSFs can derail approval. Present six to twelve months of statements with stable balances and limited negative days.

If seasonality affects your cash flow, document it and request a seasonal payment structure if available. Matching payment schedules to cash cycles strengthens your file and helps you meet credit score requirements for equipment loans by lowering perceived repayment risk.

Time in Business, Industry Risk, and the Story Behind the Purchase

Time in business (TIB) is a confidence signal. Two or more years demonstrates durability, but startups still get funded if the owner has industry experience, contracts in place, or a strong co-signer.

Underwriters also view industry risk: construction and trucking are capital-intensive but have deep resale markets; niche manufacturing or elective-care medical can be higher margin but may face reimbursement or demand swings.

Your job is to connect the dots—explain how the equipment reduces bottlenecks, increases billable hours, or opens new revenue streams. A persuasive narrative supported by quotes, purchase orders, or signed contracts can neutralize a borderline score.

Attach a pro forma showing incremental revenue, cost savings, and payback period. If the lender sees reliable cash flow from the asset, they may flex on strict credit score requirements for equipment loans to win the deal.

While numbers are key, presentation matters: neat PDFs, consistent figures across documents, and clear naming conventions speed underwriting and signal professionalism.

How to Check, Clean, and Increase Your Credit Before You Apply

Start by pulling your personal reports from the three major bureaus and disputing inaccuracies. Review derogatories, utilization levels, and age of accounts. Plan at least 60–90 days of cleanup before application if possible.

The credit score requirements for equipment loans become easier to meet when you lower revolver balances below 30%—ideally below 10%—of limits. Time payments so the statement closes with a low balance, not just the due date.

Consider requesting credit-line increases to improve utilization, but avoid opening new accounts unless strategically necessary.

For business credit, ensure your company is listed consistently with the Secretary of State, IRS (EIN), and bureaus. Open vendor lines that report (e.g., Net-30 with well-known suppliers) and pay early to build PAYDEX. Ask current vendors whether they report; many don’t by default.

Keep your business bank account active with steady deposits and minimal NSFs. When you apply, underwriters will read both personal and business credit patterns; clean files make credit score requirements for equipment loans less of a barrier and can lower your cost of capital.

Payment History, Utilization, and Inquiries—Small Tweaks, Big Gains

Payment history drives most scoring models, so automate minimums and calendar due dates. One 30-day late can dent your score for months. Utilization is the next lever you can control quickly: paying down revolving balances before the statement cut can lift your score within a cycle.

Avoid clustered hard inquiries. If multiple lenders must pull credit, try to keep inquiries within a short window; some scoring models treat rate-shopping as one inquiry, but spacing them out can cause cumulative dings.

These tactics, repeated consistently, help you clear credit score requirements for equipment loans without radical changes to your finances.

If your file contains older collections, consider negotiating pay-for-delete where appropriate and permitted. Keep documentation of any settlements to correct reporting if needed.

For thin files, becoming an authorized user on a well-managed, long-standing card can add history, though underwriters value primary tradelines more. Combine these moves with steady business operations, and your application tells a coherent story that meets both the letter and spirit of a lender’s criteria.

Strategies to Get Approved with Fair or Challenged Credit

If your score sits in the low- to mid-600s, aim to de-risk the deal. Bring a 10%–30% down payment, choose equipment with strong resale value, and limit the financed amount by negotiating price or including trade-ins.

Offer additional collateral or a co-borrower with stronger credit. Consider a shorter term to reduce total risk, then refinance later as your credit improves. These strategies help you pass credit score requirements for equipment loans even when your file isn’t perfect.

You can also pair financing with revenue proof. If the equipment is tied to a signed contract, letter of intent, or service agreement, include copies. Show insurance coverage and maintenance plans to protect the asset.

Ask lenders about seasonal or step-up payments that match cash cycles—lower payments early can ease DSCR while you ramp revenue. If approvals remain tight, explore captive finance promotions or SBA-backed options, accepting longer timelines in exchange for better structures.

The key is flexibility: adjust levers until lender risk falls within their comfort zone and credit score requirements for equipment loans become attainable.

Down Payments, Co-Signers, and Collateral—What Moves the Needle Most

Among the available levers, down payment carries outsized weight. Equity lowers LTV, cushions depreciation, and signals commitment. A co-signer with a 700+ FICO can also transform pricing, but ensure all parties understand PG obligations.

Additional collateral—like unencumbered vehicles or equipment—can help, though lenders prefer collateral that’s easy to value and liquidate. Present a clear collateral schedule with serial numbers, titles, and lien status to speed review.

Each of these offsets lets underwriters relax strict credit score requirements for equipment loans because practical protections are in place.

Don’t overlook insurance. Comprehensive coverage with lender loss-payee endorsements reduces loss severity and reassures risk teams. Provide a certificate early; it’s a small step that signals professionalism.

Finally, communicate proactively. If your file includes a late payment during a documented emergency, attach an explanation with supporting proof. Context can mitigate risk in a way raw scores cannot, helping you align with lender expectations.

Documentation Checklist to Strengthen Your File

Strong documentation can compensate for marginal credit. Prepare a complete package before you apply: government ID, entity documents (Articles, EIN letter), last two to three years of business tax returns (if available), year-to-date P&L and balance sheet, recent business bank statements (6–12 months), A/R and A/P aging, equipment quote with serial numbers, and proof of insurance or binder.

Include resumes or brief bios if industry experience is critical to performance. These items let an underwriter validate cash flow and collateral quickly, smoothing the path through credit score requirements for equipment loans.

If your business is new, replace missing history with strength elsewhere: personal tax returns, detailed business plan, sales pipeline, signed contracts, and letters from prospective clients. Keep files labeled clearly and consistent across documents.

Mismatched addresses or names create friction and re-underwriting, which can cause delays or even pricing changes. A tidy application not only increases approval odds—it also sets you up for faster funding and better terms once you meet the lender’s standards.

Underwriting Flow and Timeline—What to Expect After You Apply

After submission, expect an initial credit pull and a quick review for red flags. If your score passes the lender’s threshold, they’ll move to cash-flow analysis, verifying deposits, NSFs, and DSCR. Next comes collateral validation and UCC searches.

If everything matches, you’ll receive a conditional approval outlining rate, term, down payment, and covenants. Satisfy any stipulations—updated statements, insurance binder, or landlord waiver—and you’ll proceed to closing documents and funding.

Understanding this flow helps you align your package with credit score requirements for equipment loans, reducing surprises and speeding your path to ownership.

For larger deals, credit committees may meet weekly, so submit early and respond fast. If your score is close to the threshold, keep balances low and avoid new inquiries during underwriting.

Lenders sometimes refresh credit before funding; a sudden score drop can trigger re-price or denial. By maintaining discipline through closing, you protect the terms you earned and preserve your future borrowing power.

Tax, Legal, and Compliance Considerations (U.S. Context—Talk to Your Advisors)

Financing intersects with tax, legal, and compliance rules. Many U.S. businesses leverage Section 179 and bonus depreciation where applicable to accelerate deductions on qualifying equipment. Lease vs. loan treatment can differ for accounting and tax, so coordinate with your CPA before you sign.

UCC filings, personal guarantees, and cross-collateralization clauses are standard, but you should read them carefully and consult counsel if needed. Aligning structure with your goals ensures you meet credit score requirements for equipment loans while optimizing ownership costs.

Insurance and safety compliance also matter. For vehicles, ensure DOT compliance and proper endorsements. For medical and food-service equipment, verify FDA, NSF, or local health code requirements.

Lenders care because non-compliant assets carry higher downtime and liquidation risk. Provide certificates and inspection records early. Doing so reassures underwriters that the equipment will stay productive, which strengthens your application beyond any single score.

Protecting Your Credit After Funding—Set Up for the Next Purchase

Once you fund, set automatic payments, monitor utilization, and keep business and personal finances organized. If your lender reports to business bureaus, on-time payments can build your commercial file, easing future approvals.

Consider setting quarterly reminders to review reports and dispute errors promptly. The goal is compounding credibility: each successful loan improves your ability to surpass future credit score requirements for equipment loans, often unlocking better rates and longer terms that free up cash for growth.

If your original deal carried a higher rate due to fair credit, track your performance metrics and revisit refinancing after 9–12 months of perfect payment history. Present updated financials, a higher score, and a clean bank-statement record.

Strategic refinancing can lower costs and extend term without adding risk, putting your business on stronger footing for the next round of capital expenditure.

FAQs

Q.1: What credit score do I realistically need to qualify for an equipment loan in the U.S.?

Answer: Most lenders look for mid-600s and up, with the best pricing usually starting around 700+. That said, approvals happen below 650 when other strengths are present—bigger down payments, strong cash flow, and equipment with a healthy resale market.

Because credit score requirements for equipment loans are only one piece, underwriters evaluate DSCR, time in business, and bank-statement health.

If your score is borderline, target lenders that specialize in your asset type, prepare a 10%–30% down payment, and bring documentation that shows how the equipment generates revenue. Those offsets can win approvals even when your score isn’t perfect.

Q.2: Can I get approved for equipment financing with bad credit or recent late payments?

Answer: It’s harder, but not impossible. Alternative lenders may approve scores in the low-600s or below if the equipment is standard, the down payment is meaningful, and bank statements show stable deposits.

Expect higher rates and shorter terms at first. Focus on quick wins that lift your score: pay down revolving balances to reduce utilization, avoid new inquiries, and set up autopay to prevent further lates.

Pair those moves with collateral and a co-signer if available. Over time, you can meet stricter credit score requirements for equipment loans and refinance at better terms.

Q.3: Do equipment leases have different credit score requirements than loans?

Answer: Often, yes. Some operating leases accept slightly lower scores because the lender retains more control over the asset and expects to recover value at term end.

Finance leases and $1 buyout structures look more like loans and may require stronger credit for longer terms. Regardless of format, lenders still review DSCR, LTV, time in business, and bank-statement health.

If your credit is borderline, choose a lease or loan that matches seasonality and cash flow, offer a larger down payment, and focus on mainstream equipment with clear resale value to satisfy credit score requirements for equipment loans.

Q.3: Will a personal guarantee always be required, even for an LLC or corporation?

Answer: Not always, but it’s common for smaller deals or younger businesses. A personal guarantee aligns incentives and gives lenders a secondary source of repayment.

Removing a PG typically requires a combination of strong business credit, substantial time in business, and robust financials. In the meantime, manage personal credit diligently.

Strong personal credit can reduce rates, improve LTV, and open doors with banks and captives. Meeting both personal and business credit score requirements for equipment loans positions you to negotiate PG terms later.

Q.4: How can I boost my credit score quickly before applying?

Answer: Focus on utilization and reporting timing. Pay down revolving balances below 30%—ideally under 10%—before the statement closing date so the lower balance is what gets reported. Avoid new credit applications that add inquiries.

Bring any delinquent accounts current and set up autopay. If errors exist, dispute them with documentation. For business credit, confirm your company data across bureaus and pay vendor terms early.

These steps can lift your score within a cycle or two, improving your ability to meet credit score requirements for equipment loans without major lifestyle changes.

Conclusion

In the U.S., credit score requirements for equipment loans matter, but they’re not the whole story. Lenders approve complete packages—credit, cash flow, collateral quality, and clear business rationale.

If your score is strong, you’ll likely unlock lower rates, longer terms, and lighter down payments. If it’s fair, you can still win approvals by de-risking the deal with larger equity, proven revenue, mainstream equipment, and tidy documentation.

Choose the right lender lane—banks, credit unions, captives, online lenders, or SBA-backed programs—based on your current profile, not just your ideal one.

Think of this as a roadmap rather than a hurdle. Clean your credit reports, manage utilization, stabilize bank balances, and prepare a professional package before you apply.

Match the financing structure to your cash cycle, protect the asset with insurance and maintenance, and communicate proactively through underwriting. Do these things, and credit score requirements for equipment loans become a milestone you can consistently meet, not a barrier that blocks your growth.