Pros and Cons of Equipment Loans for Small Businesses

Equipment loans let businesses finance the purchase of physical assets by using the equipment itself as collateral. They are designed specifically for buying or upgrading equipment – anything from computers and furniture to trucks, medical devices or manufacturing machinery.

Since the asset secures the debt, lenders often offer lower interest rates and easier approval than with unsecured loans. For example, banks will finance 80–100% of an equipment purchase with typical loan terms of 3–7 years.

This allows small businesses to spread payments over time instead of paying cash upfront. In fact, about 78% of U.S. firms rely on financing (loans, leases or lines of credit) to acquire business equipment.

Equipment loans can fund many types of assets, from laptops and printers to trucks and industrial machines. The lender uses the financed equipment as collateral, which helps reduce interest costs and improve approval odds.

Because of this collateral, some equipment loans require little or no down payment (though up to ~20% down is common). An equipment loan spreads the cost over time (often 3–10 years) instead of tying up capital.

Online lenders can even approve and fund these loans very quickly – sometimes in 24–48 hours – whereas traditional banks may take a week or more. Typically the borrower makes fixed monthly payments; once the loan is paid off, the business owns the equipment outright.

This is especially valuable for durable items (office furniture, kitchen or farm equipment) that will last longer than the loan term.

Key Features of Equipment Loans

- Collateral: The equipment itself secures the loan. This reduces lender risk and often lowers interest rates compared to unsecured borrowing. Offering collateral can also help businesses with weaker credit qualify for financing.

- Loan Amount: Banks and online lenders typically finance up to 80–100% of the equipment’s value. This means a small business can acquire expensive assets without paying cash upfront.

Some loans may require a modest down payment (often around 10–20%), but many lenders offer 100% financing for qualified borrowers. - Terms and Rates: Equipment loans generally have fixed interest rates. Terms often range 3 to 7 years, though some may extend up to 10 years. Because the loan is secured, interest rates tend to be lower than for unsecured loans.

In practice, small-business loan rates in 2025 range roughly 6–12% for banks, but equipment-finance specialists may offer competitive rates (in some cases as low as ~4% APR) if credit is strong. (Rates vary widely based on credit, loan size and lender.) - Speed: Equipment loans are often funded faster than many other business loans. Online lenders can approve applications in days.

Even banks typically process equipment loans more quickly than unsecured loans, since the collateral reduces risk. Quick access to funds means a business can get new machinery or vehicles up and running without long delays. - Qualification: Lenders mainly evaluate the borrower’s ability to repay. Because the equipment acts as collateral, credit requirements are usually less strict than for standard term loans.

For example, lenders often accept a personal credit score around 600 or higher (though higher scores get better terms). They also look at business revenue, age and the asset’s value. Importantly, making on-time payments on an equipment loan can help build the business’s credit history.

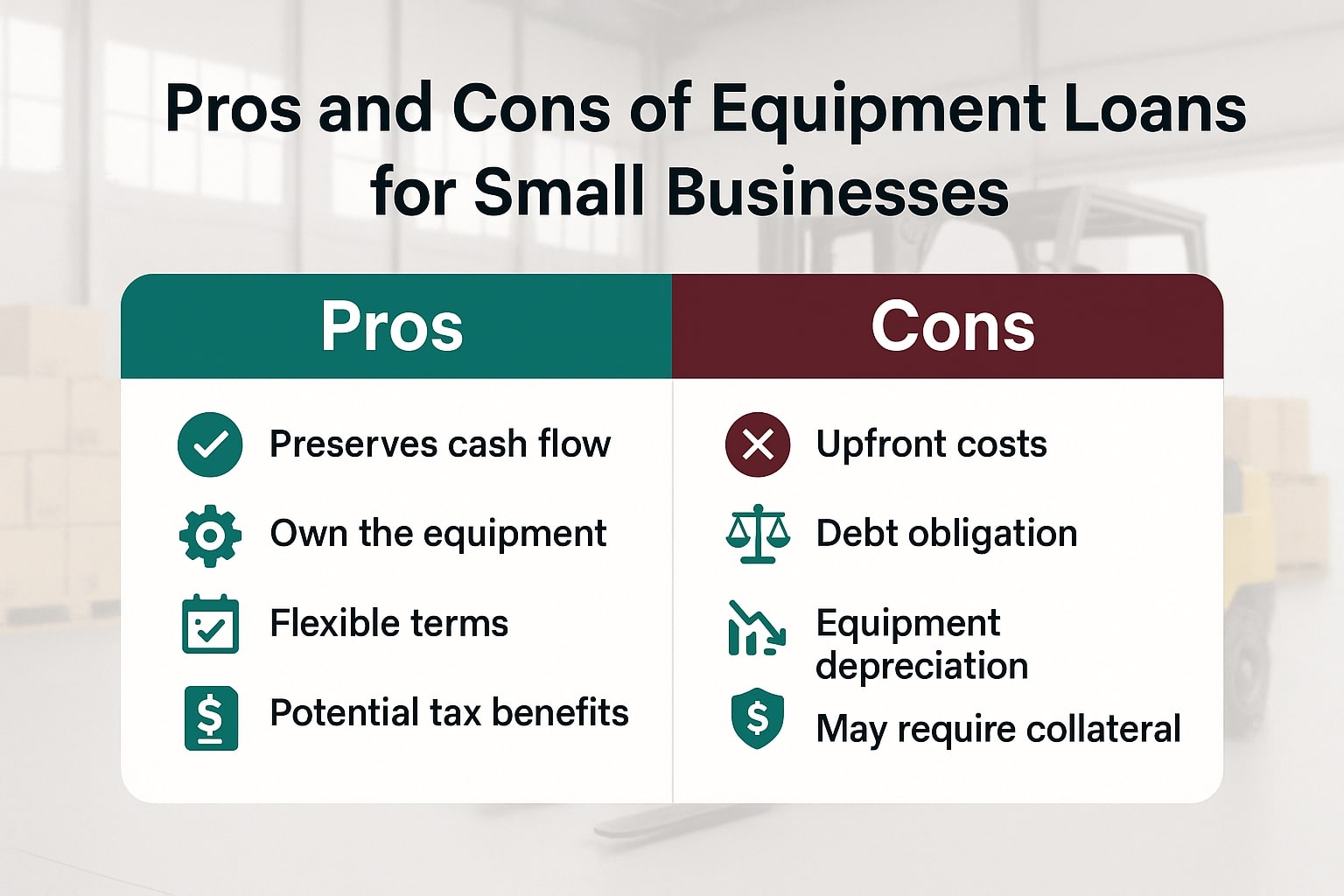

Pros of Equipment Loans. Equipment financing offers several benefits for small businesses:

- Flexible financing: You can fund almost any business equipment — from office computers and printers to heavy machinery or delivery vehicles.

Loans let you spread the cost over time (for example, 3–7 years) instead of depleting cash reserves. This flexibility helps preserve working capital for other needs. - Lower borrowing costs: Using the equipment as collateral gives lenders security, so rates are often lower than for unsecured credit cards or personal loans.

In fact, one analysis shows equipment loan approval rates (around 68%) are the highest of any small-business loan, reflecting their relative affordability. - Quick access to funds: Many equipment lenders (especially online ones) offer rapid underwriting. You may receive funds in 1–2 business days. This speed can be crucial if you need to replace broken machinery or meet a sudden opportunity.

- Build credit: Repaying an equipment loan on time can strengthen your business credit profile. Because these loans are often easier to qualify for (even for newer companies), they present a practical way to demonstrate repayment history.

- Tax advantages: The U.S. tax code (Section 179) allows businesses to deduct the full cost of qualifying equipment in the year of purchase, even if it’s financed.

For 2024 the maximum Section 179 deduction is $1,220,000 (phasing out above $3.13 million in purchases). This immediate expense can significantly lower taxable income. - Ownership at end: Unlike leasing, an equipment loan means you own the asset when the loan is paid off. Ownership can be a major advantage if the equipment has a long useful life (e.g. restaurant ovens, farm tractors). After repayment, the business retains the residual value of the equipment.

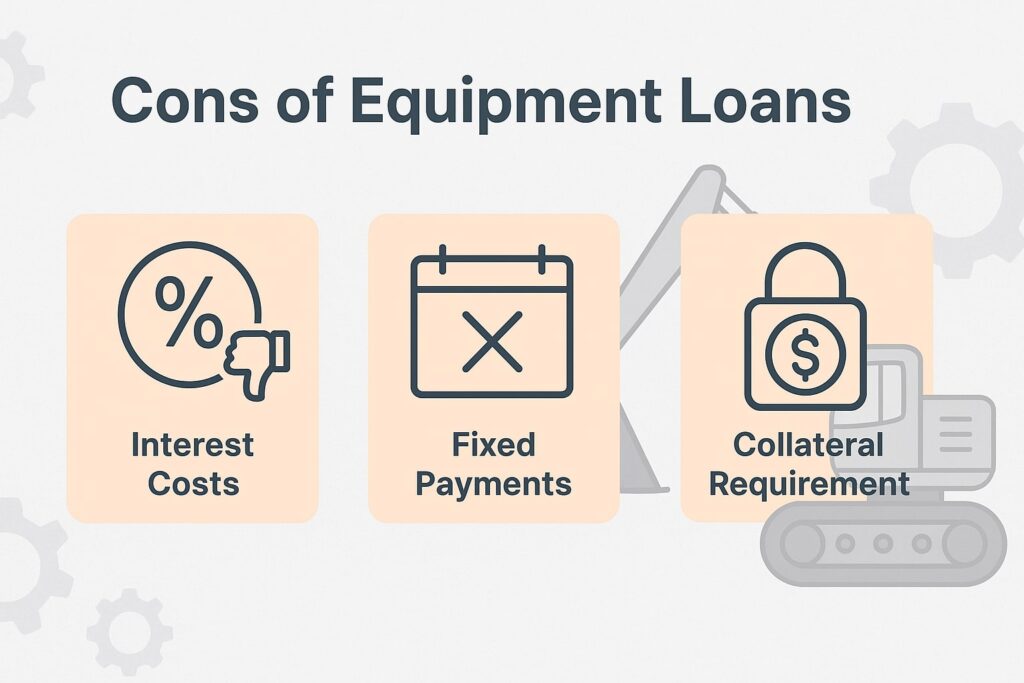

Cons of Equipment Loans

Despite the advantages, equipment loans also have drawbacks small business owners should weigh:

- Limited use of funds: By definition, equipment loan proceeds must be used for approved equipment only. You cannot divert the funds to other business expenses or inventory. If you need cash for other purposes, you’ll need a different loan or a line of credit.

- Possible down payment: While collateral helps, many lenders still require a down payment (often 10–20%) on high-cost equipment.

If you need expensive machinery, you may have to use a portion of your reserves up front. Inability to make the down payment could force you to consider leasing instead. - Equipment risk: There’s a chance the loan outlasts the equipment’s useful life. For example, if you take a 7-year loan on a copier that breaks or becomes obsolete in 4 years, you’ll be stuck paying on an asset you can’t use. You might need additional borrowing to replace or repair it.

- Extra costs: Since you own the equipment during the loan, all maintenance and repairs are your responsibility. Major breakdowns during the loan term mean extra expenses on top of loan payments. Leasing sometimes includes maintenance, but loans do not.

- Personal liability: Many equipment loans require the business owner’s personal guarantee or a blanket lien on other business assets.

This means that if the business can’t pay, the lender may go after personal or additional business property. These added liabilities increase personal financial risk. - Repossession risk: If you default, the lender has the legal right to seize the equipment and sell it to recover losses.

Any investment (payments) you’ve made is lost. To avoid this scenario, it’s critical to plan for payments carefully and maintain steady cash flow.

Equipment Loans vs. Other Options

When comparing financing choices, consider the following table of common options:

| Feature | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | Own asset after payoff | No (must return or buy out) |

| Collateral | Equipment itself (often required) | Typically none (you rent the asset) |

| Term | Typically 3–7 years | Shorter (e.g. 1–5 years) |

| Tax Deduction | Section 179 deduction allowed | Lease payments are deductible, but no 179 benefit |

| Down Payment | Often required (up to ~20%) | Usually low or none |

| Monthly Cost | Higher (owning asset) | Generally lower per month |

In general, leasing might be better if you want lower monthly payments and don’t mind not owning the equipment. Leasing usually requires little or no upfront cost, but you won’t get the tax write-off for ownership.

An equipment loan makes sense if you plan to keep the asset long-term and want the full tax and equity benefits.

Another option is a business line of credit or term loan. These can fund equipment or other needs, but often at higher rates unless secured. Lines offer flexibility, but without collateral (or even with collateral) they may have stricter credit requirements.

In the U.S., small business owners should also consider SBA-backed loans: for example, the SBA 7(a) and 504 programs allow you to purchase equipment with favorable terms and low down payments. (SBA 504 loans in particular finance long-term assets; for instance, it covers machinery with at least 10 years of useful life.)

To find the best deal, shop around and compare equipment financing from banks, credit unions, and online specialty lenders. Look at total cost (interest+fees) and consider negotiating terms.

Using high-quality equipment as collateral can often earn a lower rate. Keep in mind that better credit scores and a solid business plan usually secure the lowest rates.

Is an Equipment Loan Right for You?

An equipment loan can be a smart move if:

- You need specific equipment immediately but can’t afford to pay cash.

- You prefer owning the asset (and any residual value) rather than renting.

- You want the lowest financing costs available (collateral-backed loans often have lower APRs).

- You value tax write-offs from Section 179 (deducting the equipment cost in year one).

- You can comfortably make the monthly payments and handle maintenance costs.

If these apply to your situation, financing may help your business grow without straining cash flow. If not, or if you’re unwilling to risk using the equipment as collateral, you may consider other loan types or leasing.

Frequently Asked Questions (FAQs)

Q.1: What credit score is needed for an equipment loan?

Answer: Equipment loans are often easier to qualify for than other business loans. Lenders typically look for a personal credit score of 600 or higher, along with sufficient business revenue.

Because the equipment secures the loan, borrowers with limited history or lower scores may still qualify if other factors are strong.

Q.2: What equipment can be financed?

Answer: Almost any tangible business equipment can be financed. Examples include vehicles, heavy machinery (cranes, excavators), computers, restaurant ovens, farming equipment, medical machines, etc. Both new and used equipment are eligible with the right lender, though used equipment loans may carry higher rates.

Q.3: How are interest rates determined?

Answer: Rates depend on credit, loan size, term and the lender. As of 2025, bank term loans for small businesses average around 6–12% APR.

Equipment-specific loans can range from low single digits to 4–45% APR, reflecting differences in borrower risk and loan structure. Generally, offering strong collateral (like valuable equipment) and having good credit will get you the lowest rates.

Q.4: Is buying equipment with a loan better than leasing?

Answer: It depends on your goals. Financing (buying) lets you own the asset and claim tax deductions (Section 179), but requires you to handle maintenance and potentially a down payment.

Leasing typically has lower monthly payments and fewer upfront costs, but you never own the equipment (unless you exercise a buyout). Consider the equipment’s lifespan and how long you need it. For long-term assets, a loan often makes more financial sense.

Conclusion

Equipment loans are a powerful tool for U.S. small businesses to acquire necessary assets while preserving capital.

Pros include competitive rates, fast funding, tax breaks and eventual ownership of the equipment. Cons include limited use of funds, possible down payments, and the risk of repossession or obsolescence.

Every business is different: manufacturers, retailers, restaurants, and service firms all use equipment loans differently. Before borrowing, carefully evaluate your cash flow, interest costs and business needs.

Compare loan offers, read the fine print, and consider consulting a financial advisor. By weighing the pros and cons and planning responsibly, you can decide if an equipment loan is the right step for your small business’s growth.